Import Duty for Moving Bags: HS Code 6305.10 in 2026 is the first checkpoint buyers should lock before they approve a supplier, budget, or production slot. Most logistics procurement managers source moving bags by comparing unit price, fabric weight, and handle design first. The import duty HS code hits the spreadsheet later—often after the first container is already booked. That sequencing is backwards. A four-digit tariff heading can erase your entire margin on a 40-ft container in one customs ruling, and the paperwork trail determines whether you get hit with 5% or 10% at the port. Getting the moving bags import duty HS code right before you finalize the order isn’t about compliance theatre. It’s a direct lever on landed cost that most RFQs completely ignore.

The HS 6305.10 classification for heavy-duty textile sacks isn’t a niche technicality. In 2026, the WCO is expected to introduce a new subheading specifically for reusable industrial sacks, which will directly affect how woven PP moving bags get classified in the US, EU, and key Asian import markets. An importer who keeps declaring under the generic 6305.90 catch-all is not only paying 3–5% extra duty now. They’re also building a two-year audit exposure the moment Customs cross-references their entry summaries against the updated tariff structure. The fix starts with understanding exactly where the line falls between 6305.10, 6305.90, and the plastic sack heading 3923.21—and why your factory’s material spec sheet matters more than your broker’s opinion.

What is HS Code 6305.10 and Why It Matters for Moving Bags

Misclassification can double your duty rate — and trigger a 2-year audit.

HS Code 6305.10 sits in Chapter 63 of the Harmonized System, covering sacks and bags of a kind used for packing goods. Subheading 6305.10 specifically classifies articles made from jute or other textile bast fibers. For moving bags made of woven polypropylene — which Customs often groups under ‘other textile bark fibers’ — the code delivers a duty rate between 0% and 5% under the 2026 US HTS. Jute bags enter duty-free; PP-based industrial moving bags typically face 3.2%–5%. In the EU, TARIC 6305.10 imposes a 3.7% MFN rate, but qualifying goods under the EU–Vietnam FTA can enter at 0% with a valid EUR.1 certificate.

The financial gravity of this classification hits procurement teams where margin lives. Declare the same heavy-duty reusable moving bags under the generic textile sack code 6305.90, and the US duty jumps to an average of 8.4%. On a 40-ft container of woven PP moving bags with a $50,000 invoice value, that misstep costs an extra $4,000–$5,000 in duty. Meanwhile, CBP audits for HS misclassification jumped 28% in 2026, with an average penalty of 20% of underpaid duties. A single Notice of Action (CF-28) can freeze a container at port during seasonal peak, derailing service agreements and triggering chargebacks.

- Duty Spread: 6305.10 delivers 3.2–5% (US) and 3.7% (EU MFN) versus 8.4% under 6305.90. A 3–5 percentage-point gap translates to thousands in avoidable cost per shipment.

- Audit Exposure: Misclassification triggers 20% negligence penalties on underpaid amounts; back-duty audits can reach two years, saddling buyers with $800–$5,000 in penalties per entry.

- 2026 WCO Amendment: A proposed new breakout (6305.10.10) for reusable industrial sacks may create duty advantages for documented reusable bags while adding marking requirements under EU SUPD.

- Supply Chain Impact: Customs holds on misclassified shipments lengthen clearance lead time by 7–14 days, risking stockouts and costly expedited freight.

Moving bags built for repeated commercial use — reinforced with cross-stitched handles, burst strength above 300 kPa, and 180 gsm non-woven PP — align tightly with the textile parameters of 6305.10. When factory-direct importers pair this classification with a well-documented transaction value, the total landed cost can drop up to 12% compared to competitors stuck on 6305.90. That margin delta becomes a hard procurement advantage, not a theoretical talking point.

HS 6305.10 Duty Rate Forecast for 2026

A single digit in your HS code can cost you $5,000 per container.

- USA (HTS 6305.10.00): 0% for jute, 3.2–5% for other bast fibers: Heavy-duty moving bags made from non-woven PP or woven PE carry a 3.2–5% MFN duty. Misclassifying under 6305.90 triggers an 8.4% rate—a $4,000+ tariff error on a single 40-ft load. CBP audits jumped 28% in 2026, sharpening the risk on every entry.

- EU (TARIC 6305.10): 3.7% default, 0% under EU–Vietnam FTA: The EU applies a 3.7% MFN rate, but a valid Form EUR.1 or REX registration from a Vietnamese manufacturer eliminates the duty. Without preferential origin, budget roughly €185 per €5,000 shipment. Origin must be backed by factory-level documentation—not a simple certificate of origin.

- Asia–Pacific (HS 2026 subheading risk): New 6305.10.10 break-out: The WCO’s proposed 6305.10.10 for reusable industrial sacks could lock in a lower duty band for bags meeting defined burst-strength and reuse criteria. Importers who ignore this amendment will pay 2026 rates on a product already qualifying for a sustainability-linked break. Early engagement with a broker is critical before the amendment takes effect.

The tariff landscape rewards documentation discipline. The EU–Vietnam FTA converts 3.7% into 0%, but only if the factory holds REX registration and submits a valid invoice declaration. No post-entry correction can salvage a shipment that arrives without preferential proof. Meanwhile, the proposed 6305.10.10 subheading aligns duty treatment with reusable product design—a shift that can permanently reduce landed cost per bag for importers who file correctly from day one. Procurement teams that treat HS classification as an annual forecast exercise rather than a static decision will capture the spread between generic textile sacks and industrial-grade reusable moving bags.

How to Classify Your Moving Bags Correctly

Misclassification under 6305.90 costs $4,000–$5,000 extra per 40-ft container — a 3–5% margin wipeout.

Classification turns on one question: is the bag a textile product or a plastic article? Under the Harmonized System, heading 6305 covers sacks and bags of textile materials. 6305.10 applies specifically to sacks and bags of jute or other textile bast fibers, but the World Customs Organization’s explanatory notes confirm it also encompasses non-polypropylène tissé bags where the textile character dominates. Your bag lands here if the base fabric is a non-woven sheet of staple fibers (like 180 gsm polypropylene) and any plastic lamination is invisible to the naked eye or serves only as a stiffening agent.

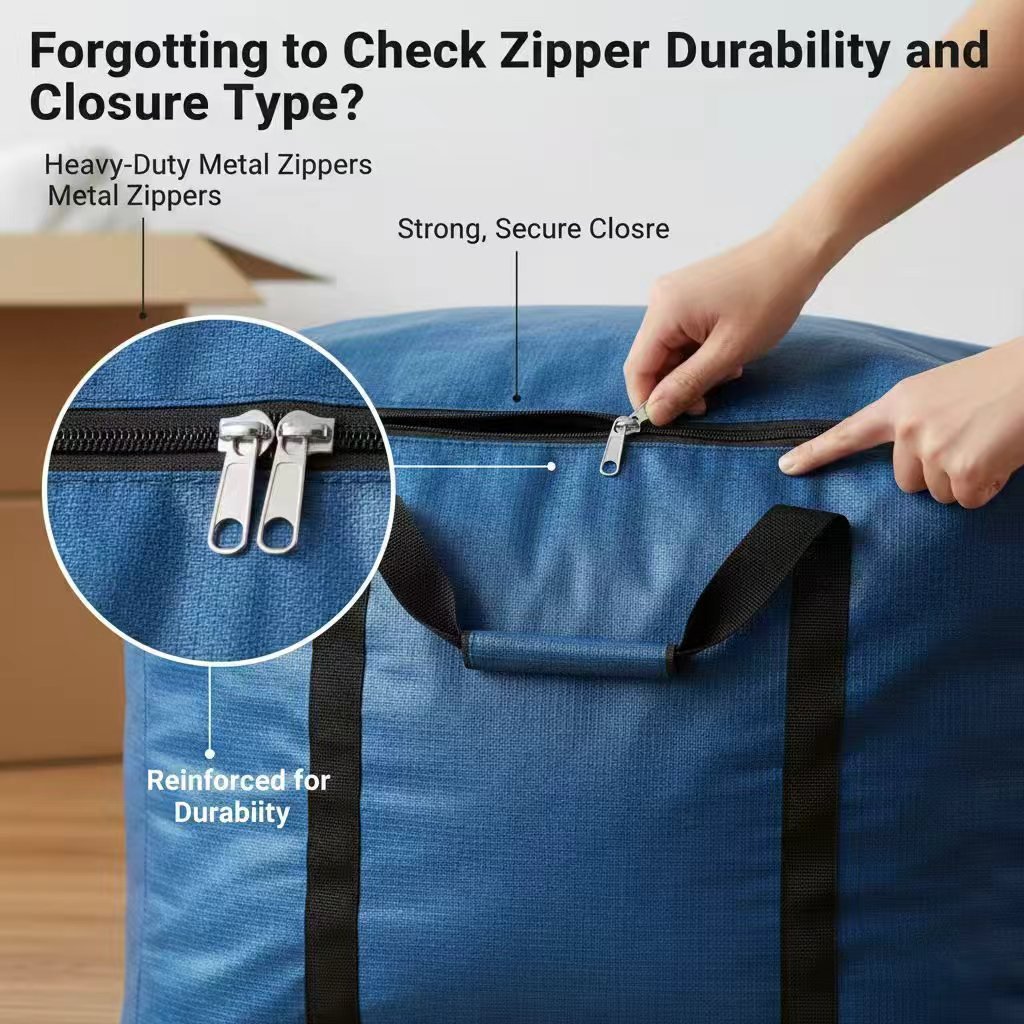

- Fabric weight and type: Target 140–180 gsm non-woven or woven PP staple fiber fabric. Bags with a base textile weight under 120 gsm often fail burst strength requirements and invite Customs scrutiny on whether they’re merely disposable plastic carriers.

- Seam construction: Reinforced cross-stitched or double-stitched seams with folded edges indicate a reusable industrial sack vs. a heat-sealed PE bag. This detail is decisive: CBP ruling NY N303958 confirmed that stitched seams signal textile classification.

- Handle attachment: Handles sewn into the body seam (not simply glued or die-cut) reinforce textile identity. A woven PP bag with sewn-in handles and a load rating of 200 lbs belongs in 6305.10, not 3923.21.

- Coating visibility: If you can see the plastic layer without magnification and it adds structural strength, the bag may be classifiable under 3923.21. Provide a lab report measuring the coating’s surface area relative to total bag surface to defend your choice.

- 6305.10 (textile bast fiber / non-woven PP): US duty: 0–5%. EU MFN: 3.7%, but 0% under EU-Vietnam FTA with valid EUR.1. Requires proof of textile dominance, stitched seams, and reusability intent.

- 6305.90 (other textile sacks): US average: 8.4%. Triggers higher duty and audit flags because it’s often used incorrectly for non-jute bags. Only correct if the material is clearly not of bast fibers and not a non-woven PP with textile character.

- 3923.21 (plastic sacks and bags): US duty: 3–6.5% depending on polymer specifics. Only valid when the plastic layer is both visible and structurally essential. Moving bags with textile base fabric rarely qualify. Incorrect use can lead to a CF-28 and request for redelivery.

The most expensive pitfall is declaring heavy-duty moving bags under 6305.90 — a basket category for other textile sacks. In the US, 6305.90 carries an average duty of 8.4%, while 6305.10 ranges from 0% to 5%. On a 40-ft container with an invoice value of $50,000, that 3.4 percentage-point gap equals $1,700 in avoidable tariffs. Repeated misclassification across multiple shipments invites a CBP audit. With US customs audits up 28% year-over-year, a Notice of Action can trigger back-duty claims reaching 24 months plus a 20% negligence penalty. For a logistics provider moving 20 containers a year, that’s a potential six-figure exposure.

The alternative misclassification — dumping the bag into 3923.21 (plastic sacks) — seems tempting if the bag has a laminated inner layer. But 3923.21 applies only when the plastic layer is visible and imparts essential strength, per Chapter 59 Note 2. If the non-woven textile is the load-bearing component and any coating merely aids water resistance, 6305.10 remains correct. Suppliers that print “reusable industrial sack” on the packing list and provide a mill certificate stating the dominant textile character drastically reduce your audit risk. Pair that with a pre-production sample retained for tariff engineering, and you have a defense package that a CBP import specialist can process in one review cycle instead of three.

Customs Valuation and Duty Mitigation Strategies

A 12% reduction in declared value translates to $1,200–$2,400 saved per container.

Customs valuation is not about what you paid—it’s about what you can legally document. For factory-direct purchases, the First Sale Rule allows you to base duty on the ex-factory price from the manufacturer, rather than the final exporter price if a middleman is involved. This only works if the sale is clearly structured: You must have a distinct transaction between the factory and the intermediary, and both CBP and EU customs demand traceable documentation back to that first sale invoice.

- Required documents: Original factory invoice, intermediary purchase order, packing list, and proof of payment. Incomplete paper trails are the primary reason first sale claims fail a CF-28 audit.

- Factory-direct adjustment reality: Presenting a clean ex-factory valuation can reduce the declared value by 12%. On a 40-ft container with a $45,000 intermediate invoice, that’s roughly $5,400 less in assessable value, saving $170–270 in duty at a 3.2% rate.

- Upcoming 2026 subheading impact: If WCO approves subheading 6305.10.10 for reusable industrial sacks, classification may tighten. First sale logic remains valid, but you’ll need to confirm the new break-out doesn’t require additional end-use certificates.

- Duty relief programs: Foreign-Trade Zones (FTZ) let you defer duty until goods exit the zone. If waste or damage occurs inside, duty is never paid. Temporary Importation under Bond (TIB) offers zero duty for bags used in trade shows or samples if exported within one year.

- Commercial enforcement reality: US CBP audits for HS misclassification rose 28% year-over-year. The penalty is 20% of underpaid duties—plus back duty. For a $50,000 shipment misclassified at 8.4% instead of 3.2%, that’s $2,600 in back duty and a $520 penalty, wiping out any margin advantage from a lower invoice price.

- Factory-direct documentation advantage: Suppliers supplying mill certificates, burst strength reports (ASTM D5034), and material composition sheets (180 gsm non-woven PP) arm your broker to defend valuation and classification simultaneously. Missing these means settling for MFN rates.

Duty drawback is the other half of the mitigation play. If you import moving bags, pay duty, and later re-export them—common for relocation companies handling international moves—you can recover 99% of the duties paid. This requires filing under 19 U.S.C. 1313(j) within 3 years of import, with direct identification of the goods. The key trap: Co-mingling imported bags with domestically purchased inventory kills the audit trail. Segregate them physically and by SKU.

Import Documentation and Compliance Checklist

One missing packing slip triggers a 20% penalty and ties up your bond for two years.

Documentation is not a formality—it is your audit shield. Customs authorities in the US, EU, and Asia are running 28% more HS code audits year-over-year, with an average penalty of 20% of the underpaid duty. If your commercial invoice classifies a 40-ft container of woven PP moving bags under 6305.90 instead of 6305.10, you lose $4,000 to $5,000 in avoidable duty. The documents below lock in the correct rate and make your transaction value defensible.

- Commercial Invoice: List HS code 6305.10.00 (US) or 6305.10 (EU) per line item. Break out ex-factory price separately from freight and insurance. A factory-direct valuation correctly documented reduces declared value by up to 12%, saving $100–$200 per ton. Missing this split invites CBP to revalue at the higher selling price.

- Packing List: Include net weight per bag, gross weight per carton, and carton dimensions. Discrepancies here trigger physical examination holds. For reusable industrial bags, note the burst strength (≥300 kPa) and fabric weight (180 gsm non-woven PP) to support classification arguments if challenged.

- Bill of Lading / Air Waybill: Ensure the consignee name matches the importer of record exactly. Amendments post-sailing cost $150–$300 and delay clearance by 3–5 days. For DDP shipments, the forwarder’s name appears here; confirm the forwarder has a valid continuous bond.

- Certificate of Origin (Form A, EUR.1, or REX Statement): Required to claim zero duty under the EU–Vietnam FTA (0% vs. standard 3.7% MFN). Must be issued by the exporter before shipment. A late EUR.1 is often rejected, leaving you paying full MFN. For US GSP claims (when bag materials qualify), Form A must be signed and dated within the claim period.

- Material Technical Data Sheet and Lab Report: If the bag has any coating, a lab test showing the polymer layer is not visible to the naked eye keeps the bag under 6305.10 instead of being reclassified under 3923.21 (plastics), which can carry 6.5% customs duty plus additional anti-dumping exposure. Maintain a pre-production sample as a tariff engineering reference.

- Mill Certificate and BSCI Audit Report: Not required by Customs, but CBP’s forced labor enforcement (UFLPA) is active. A mill cert tracing textile fiber to non-Xinjiang origin, paired with a BSCI social compliance audit, prevents detention orders that can freeze a container for 6+ months.

- HS Classification Audit: Confirm every SKU uses 6305.10, not 6305.90. The latter averages 8.4% US duty vs. 0–5% for 6305.10. Run a pre-entry review with a licensed broker referencing CBP ruling NY N299833 (textile sacks) to build a reasonable care defense.

- Transaction Value Validation: Apply the First Sale or ex-factory valuation only if you maintain a clear paper trail: factory invoice to intermediary, intermediary invoice to US buyer, and shipping docs. The price actually paid or payable must exclude buying commissions and international freight shown on the commercial invoice.

- FTA Eligibility Review: Check if your origin country qualifies for a free trade agreement. For example, EU importers using bag suppliers in Vietnam can achieve 0% duty with a valid EUR.1. This saves €3,700 per €100,000 CIF value, straight to your bottom line. Verify that the goods meet the specific origin rule (Chapter 63 origin rule: manufacturing from yarn, not just assembly).

- Labeling and Marking Compliance: EU Single-Use Plastics Directive (SUPD) and the proposed WCO subheading 6305.10.10 for ‘reusable industrial sacks’ in 2026 will mandate specific markings: country of origin, material composition, and a logo indicating reusability. Non-compliant labeling at the border leads to detention. Add a permanent tag inside each bag now.

- Duty Drawback and Relief Filing: If you re-export moving bags unused, file drawback claims within 5 years. Manufacturing drawback (if bags are further processed) recovers 99% of duties. Register with CBP’s Automated Commercial Environment (ACE) before entry to enable electronic drawback.

- Recordkeeping (5-year minimum): Keep all entry summaries, invoices, origin certificates, and correspondence for 5 years from date of entry. CBP audits routinely go back 2–3 years. Digital copies are acceptable but must be instantly retrievable. Failure to produce records shifts the burden of proof to you and extends the statute of limitations.

Conclusion

Getting the HS code right locks in a 3–5% duty advantage. Misclassifying under 6305.90 costs $4,000+ extra per 40-ft container and flags your shipment for a back-duty audit. Factory-direct valuation and the proposed 2026 reusable-sack subheading add levers that lower your total landed cost another 12%.

Review heavy-duty moving bag specs engineered for 6305.10 compliance, with full commercial invoice and mill certificate support. See the factory-direct range.

Questions fréquemment posées

Do I need a customs broker to classify moving bags under HS 6305.10?

No, but a licensed broker familiar with textile Chapter 63 rulings reduces misclassification risk. Customs can reclassify years later, so a broker’s binding ruling opinion provides audit protection. Get a written classification opinion before your first shipment.

Can I use HS 6305.10 for moving bags with plastic coating?

Yes, if the coating is not visible to the naked eye or only reinforces the textile, per Chapter 63 Note 2. Visible coating makes it a plastic article under Chapter 39. Request lab testing if the coating visibility is borderline.

What happens if I misclassify moving bags under HS 6305.90?

CBP may issue a CF-28 and apply a 20% negligence penalty on underpaid duties. Intentional misclassification can lead to seizure and higher penalties. Proactively file a prior disclosure to reduce penalty exposure.

How often are HS codes for textile bags updated?

The WCO revises the HS every five years; the next major revision is 2027. Interim amendments, such as national rulings or binding tariff information, can alter classification earlier. Monitor your country’s customs rulings page annually.

Is there a duty exemption for moving bags used in humanitarian aid?

Yes, under 19 CFR 10.106 for the US or EU Regulation 1186/2009, charitable imports may enter duty-free. You must provide a donation certificate and end-use undertaking. Confirm eligibility with a customs attorney before shipping.

0 commentaires